With more than 10 years of experience in the valuation and consultancy of intellectual property, companies, and entrepreneurial risks, I took the step into independence in order to realize my own ideas of a modern boutique consultancy in IP valuation and economics.

The valuation of assets and operational decisions under risk are the most interesting fields of applied economics, with intangible assets and intellectual property the "supreme discipline". They are almost always incomparable to other economic goods or require careful adjustment and consideration.

In the valuation of intangible assets, economic knowledge and intuition are therefore regularly required, and often also the courage to find and defend new solutions.

But we are standing on the shoulders of giants: questions of IP valuation have interested the best economists and regularly concern the courts. It is therefore necessary and a sign of respect to know the solution approaches others have tried before.

Nobody can be an expert on everything. As an affiliate consultant at NERA Economic Consulting, I have access to a global network of economic experts, so I can find the best solution for you even in the most complex cases when (IP) valuation, competition, industry regulation and other issues overlap.

based on recognized valuation standards (IDW S5, DIN ISO 10668, DIN 77100, IVS 210)

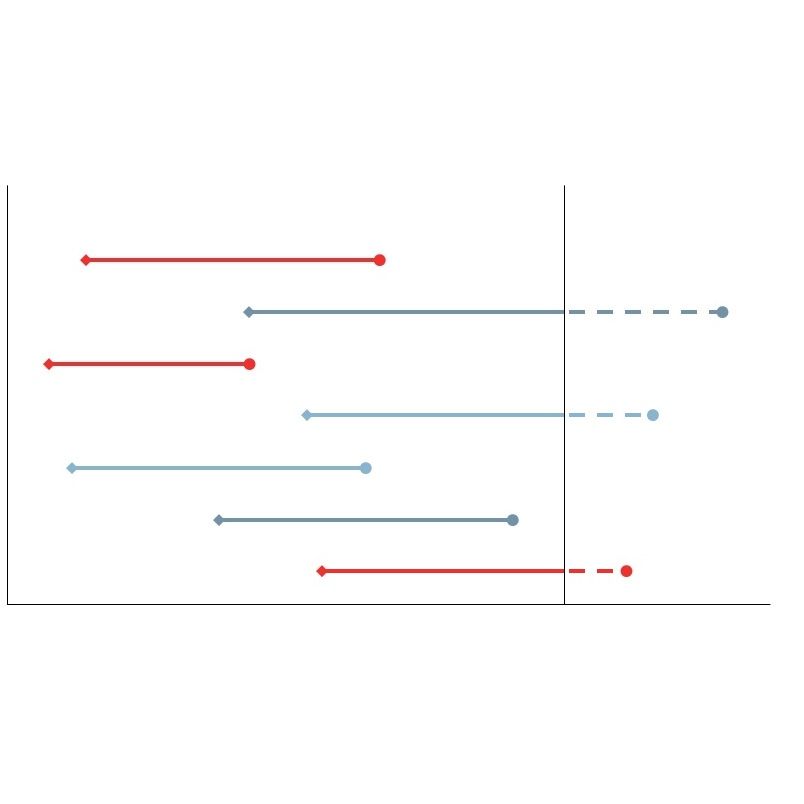

In the picture: measuring the lifespan of product brands

e.g. customer base, user base, workforce, trade secrets

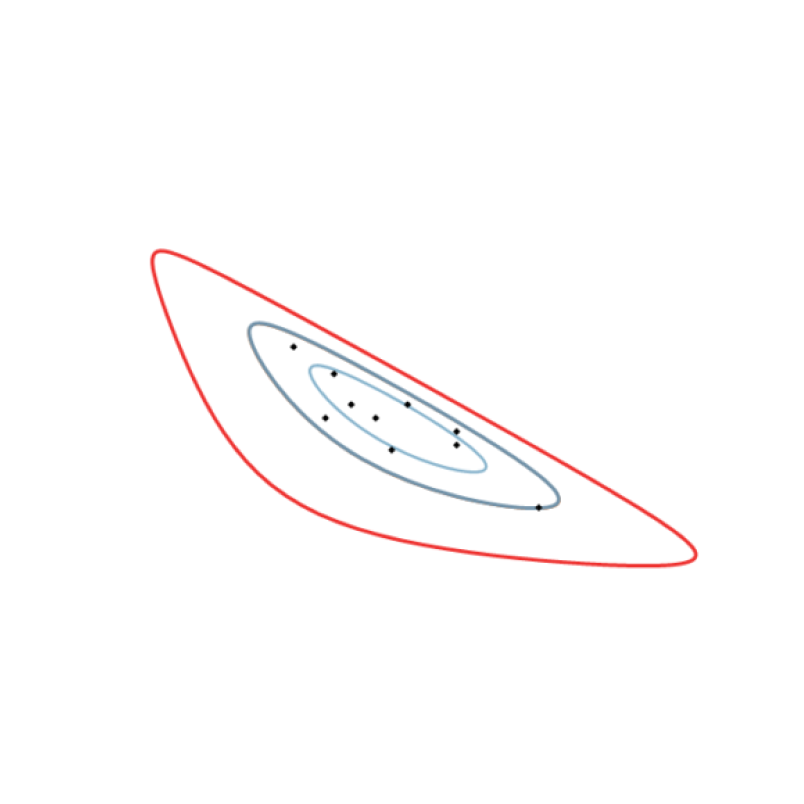

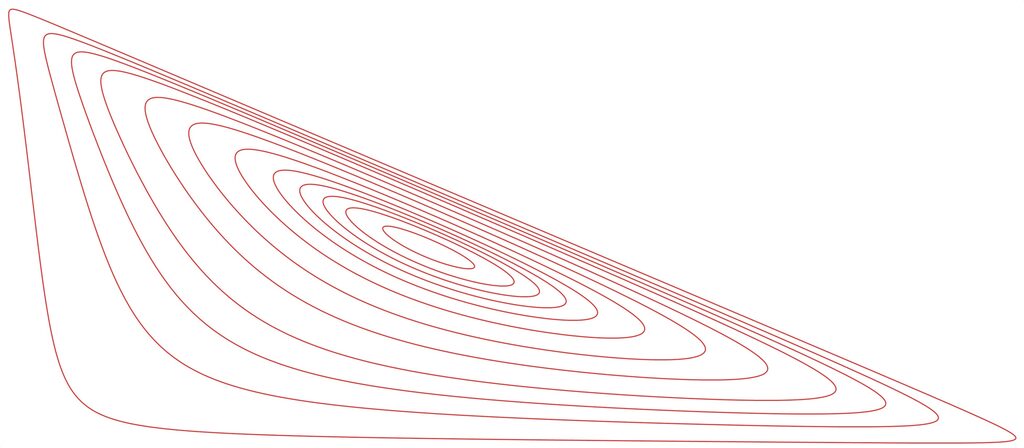

In the picture: Profit distribution among three parties and statistically determined confidence regions.

ZE.g. in the context of relocation of functions and exit taxation

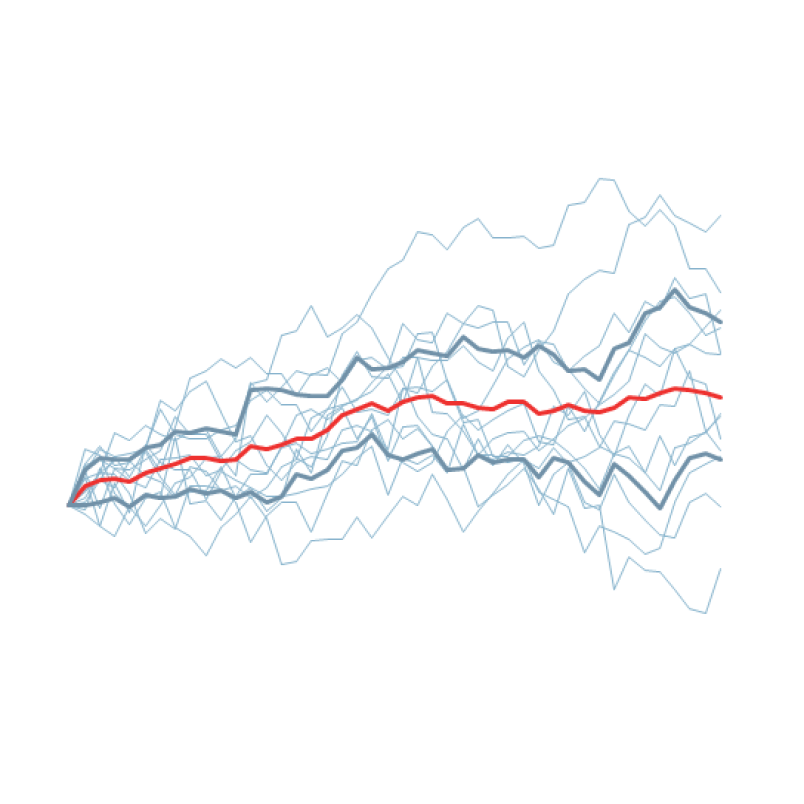

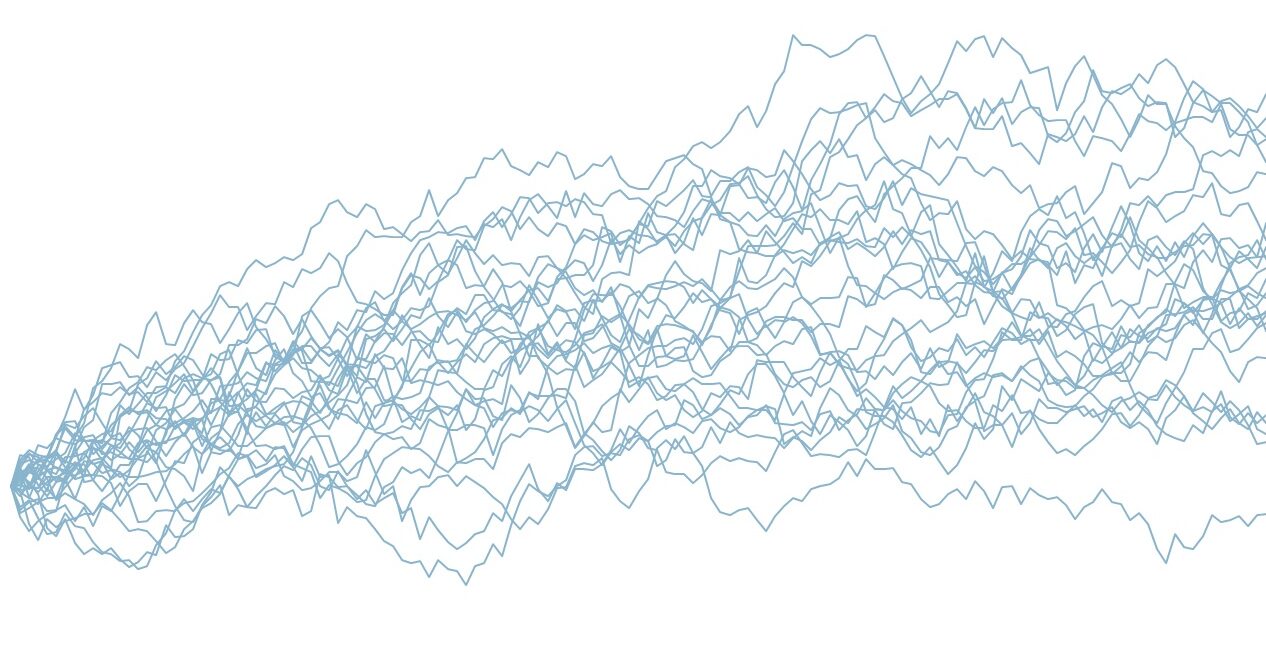

In the picture: Monte Carlo simulation of a market price trend with mean reversion, typical for commodity prices

In damage cases , especially with respect to lost profits, it is important to present the opportunities and risks of the valuation object of and the industry in a consistent economic framework. Hereby help:

in the picture: modelling of subscription churn with constant and heterogeneous churn rate

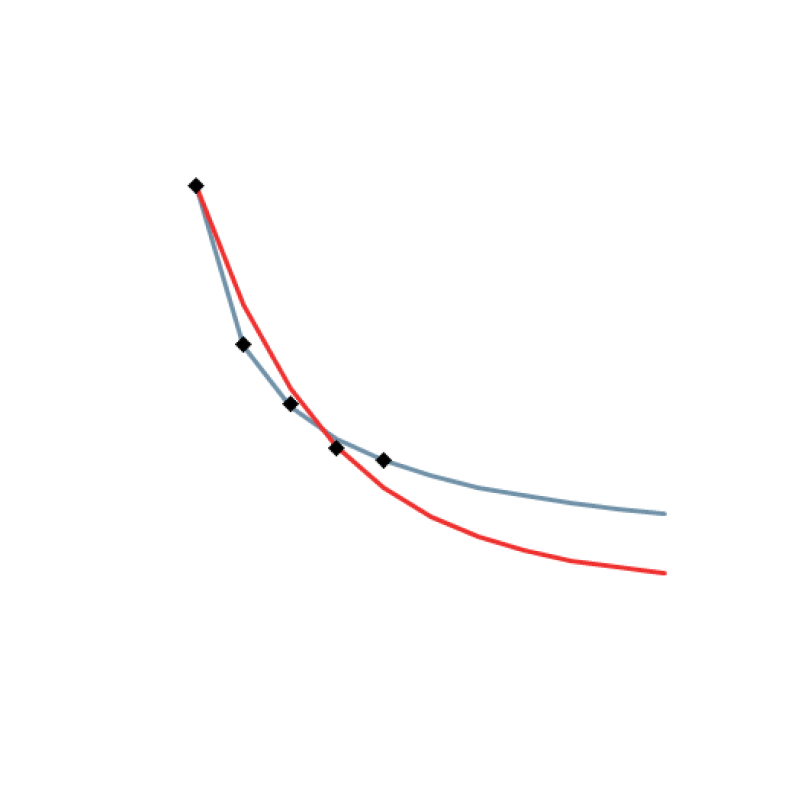

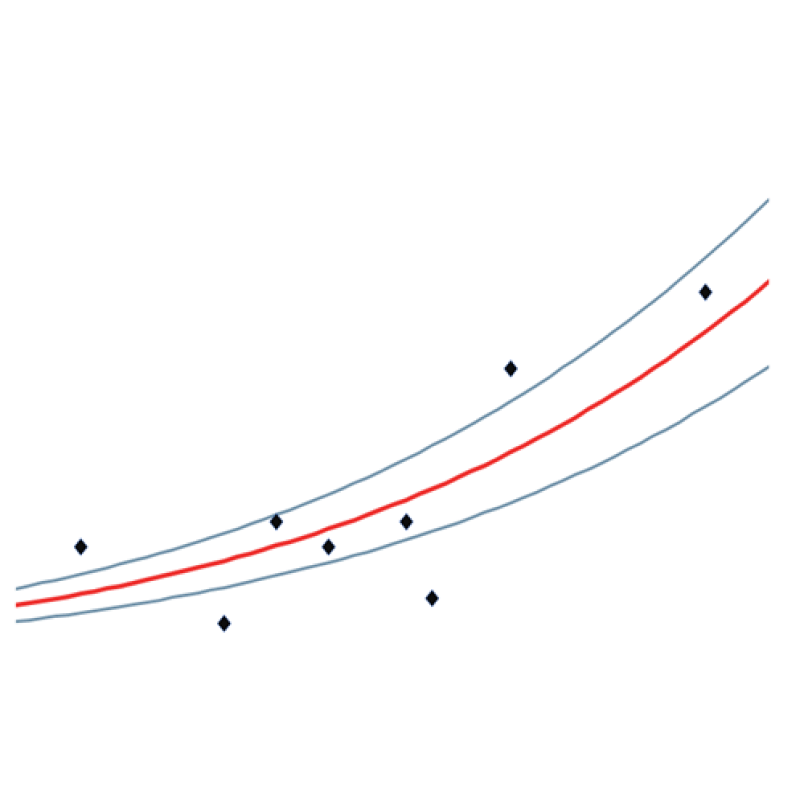

in the picture: non-linear, logistic adjustment calculation to licence rates with confidence interval

in the picture: Significance analysis of risk premiums using the bootstrapping method

The valuation of intellectual property (IP) and intangible assets can only rarely be exercised in a fixed, standardized valuation concept.

The value of:

patents stems precisely from the fact that something new is made or made in a new way,

brands comes from being different than the others,

and the value of company secrets comes from things others do not know.

As a rule, these valuations are associated with greater uncertainty than classic company valuations.

Luckily, one is not in the wilderness when it comes to these valuation problems. The difficulties of valuation have also drawn the brightest minds in economics into valuing intellectual property. As the best example of an interdisciplinary applied science, the valuation of intangible assets can also adopt methods from other research areas in order to find solutions to difficult questions.

Almost every company has some form of intangibles and these continue to grow in importance. It is all the more important for the company valuation to consistently consider the valuation peculiarities of intellectual property.

As nice as it can be to perform a valuation in an ideal world, clients typically need the valuation for very specific purposes. Associated with these purposes are standards, guidelines, landmark court decisions, essays, and common established practice.

A valuation that respects the client's needs can only be performed if one knows how the explicit and implicit assumptions of the models what the alternatives are. And also, if one knows when to consciously choose a different path than the well-trodden.

In dispute resolution cases, for optimal outcome it is necessary that client, legal counsel and economic advisor/valuation expert form a triad. This can only succeed if the valuation expert understands the background to the legal advisor's strategic approach, or even anticipates it. Without diminishing highest standards of independence, objectivity and scientific approach, a good valuation never stands alone, but is integrated into the surrounding landscape.

It is therefore particularly important to me, for example as a member of the LES (Licensing Executive Society), to be in regular contact with patent and trademark attorneys and other specialists in the field of intellectual property. As an Associate Consultant at NERA Economic Consulting, I am also part of a global network of economic experts who are leaders not only in intellectual property, but also in transfer pricing, energy, competition and regulated markets.

Especially when it comes to intangible assets, no two cases are the same. Therefore, what is required is

empathy for the client's needs, and willingness to listen,

creativity in finding solutions, and appreciation for other, contradictory approaches,

as well the passion to present solutions in an aintuitive and plausible manner.

Contact me about how I can help you!

with Dr. Alexander Vögele in

The OECD requires that adjustments to comparable contracts in licensing or profit splits are sufficiently reliable (2022 OECD Guidelines subs. 6.129). But to be reliable, adjustments should at least respect the natural economic boundaries of royalties and profit splits, namely that a) royalties and profit split shares are not negative and b) that the shares of all parties sum to exactly 100%.

While this is trivial, creating statistically correct adjustments for high or low royalties and split shares becomes difficult. Luckily, similar problems occur in biology and the social sciences, so "logistic regression" as reliable statistical method has been devised and also implemented in several programming languages. We show how this can be applied to royalty adjustments and adjustments to a three-party profit split. In a follow-up article, we show how this can be achieved in spreadsheet programs like Excel.

with Dr. Alexander Vögele in

In transfer pricing, there is regularly a need to perform adjustments on royalty rates obtained from comparable uncontrolled transactions. In our previous article,we showed how reliable adjustments can be obtained by logistic regression. This ensures that the adjustment observes the natural economic boundaries of royalties: a) the shares of the respective partners should each be positive; and b)sum to 100 percent.

The influence of these boundaries is also important in their vicinity: License rates bend near the natural limit of 0 percent and will reach 0 percent only in the infinite limit. Adjustments should have a nonlinear form as in the figure. In this article, we provide a step-by-step approach of how to perform the adjustments for logistic regression.

with Dr Alexander Vögele in Vögele/Borstell/van der Ham: "Transfer Pricing - Business Administration, Tax Law", 6th edition 2023, C.H.Beck

In this basic microeconomic chapter, we show how standard microeconomic tools (supply and demand curves, price elasticities, marginal and average costs) can be used to determine arm's length prices. The industry and competition analysis - unfortunately often only treated superficially in transfer pricing documentation - is of enormous importance for the long-term understanding of prices and the profits affected by transfer pricing.

with Dr Yves Hervé in Vögele (ed.): "Intangibles - Intangible Values", 2nd edition, C.H.Beck

While DEMPE (Development, Enhancement, Maintenance, Protection, Exploitation) is now firmly established for the attribution of intellectual property, the question remains of how these contributions can be quantified. In this article, we show how this can be done for the individual DEMPE categories using economic analyses, for example to determine the platform value, for the distribution between preservation and protection of intangibles or between hardware, software and customer-centric services. Although these analyzes are of an economic/statistical nature, they are intuitively understandable and can be transferred to other situations with appropriate adjustments.

with Dr Yves Hervé in TPI-Transfer Pricing International 04/2018, Linde-Verlag

On June 21, 2018, the "Inclusive Framework on BEPS" published the final version of the revised guidance on the application of the transactional profit split method. While the changes in the main part were relatively minor, the OECD made significant improvements to the examples, and thus at least partially provided further clarity.

However, some vagueness remains, which on the one hand lies in the nature of the method and on the other hand will unnecessarily create ambiguity and uncertainty in the application of the profit splitting method in the future.

with Dr Yves Hervé in Vögele (ed.): "Intangibles - Intangible Values", 2nd edition, C.H.Beck

We show how beneficial ownership can be assigned in accordance with the OECD guidelines, based on the negotiating power of the legal entities in committees or steering committees. We explain the "Banzhaf power index", a solution concept taken from political game theory and adapted for hierarchical systems. In some cases, it is found that committee members with a small share of the vote - even if they make DEMPE contributions - often have no control over the intangible and therefore cannot be real co-owners of the intangible. But a case-by-case analysis of the decision-making structures remains essential for determining economic ownership.

with Dr Alexander Vögele in Vögele (ed.): "Intangibles - Intangible Values", 2nd edition, C.H.Beck

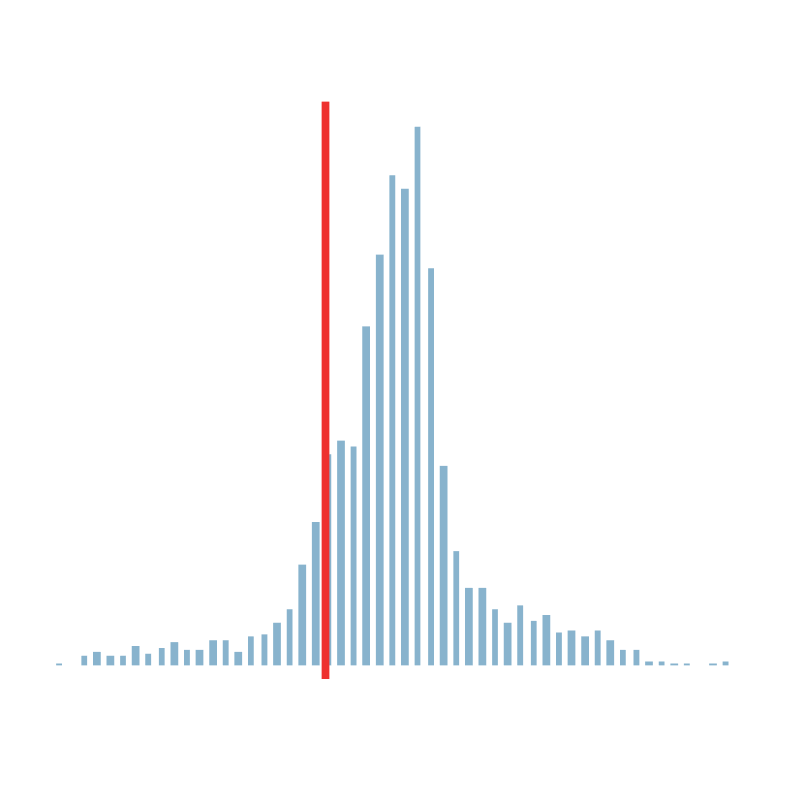

The remaining useful life of intellectual property is one of the biggest factors influencing the value of intangible assets, but at the same time it is associated with great uncertainty. Auxiliary figures, taken from tax law or patent law, are usually of little help. In some cases, however, lifetimes can be determined using statistical methods. The same methods can be used here as are used regulary in medical statistics to estimate the survival time of patients or in engineering to study the time-to-failure of critical elements.

Using an example of recipes, we show how the expected remaining economic life of recipes can be determined and that the statistically sound estimate differs significantly from naive statistical approaches.

gele (ed.): "Intangibles - Intangible Values", 2nd edition, C.H.Beck

In this article we show that there are usually natural economic limits for license rates and profit split shares: These are greater than zero and the shares must add up to 100%. However, this trivial property makes adjustment calculations much more difficult, especially in the case of low license rates and profit splits with more than two parties. Still, "reliable" (OECD-RL 6.129) adjustment calculations should take this into account. But as we show, reliable results can be obtained using "logistic regression", a method widely used in the natural sciences. In an example, we guide the reader step by step through the method so that it can also be understood by "economic laypersons" and reproduced in Excel.